On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act (TCJA), marking the first significant reform of the US federal tax code for individuals, small businesses, and corporations since the 1986 Tax Reform Act.

Beginning in 2018, the TCJA provides several tax-saving opportunities for businesses of all shapes and sizes and—most notably—a new tax deduction for small business owners (pass-through entities).

In this article, some highlights of the TCJA will be discussed, but please beware. Although the TCJA was hawked as a simplification of our taxation process, many experts tend to disagree. Seek the advice of a financial advisor to obtain optimal tax benefits for you, your family, and your business.

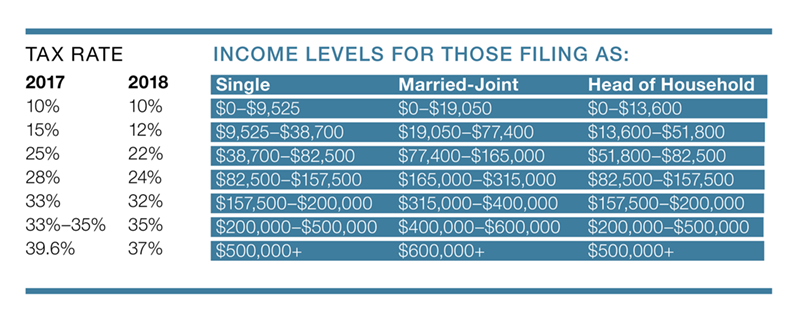

Individual Tax Brackets

Beginning in 2018, there are still seven tax brackets for individuals, but rates for several brackets are lower. Taxpayers will be placed in one of the following seven tax brackets, based on income:

Corporate Tax Bracket

The graduated tax rate structure for corporations, which featured a top tax rate of 35 percent in 2017, is being replaced by a flat rate of 21 percent. As a result, the overall tax liability of many C corporations will be reduced, and the alternative minimum tax (AMT) for corporations has been eliminated altogether. Due to the new flat rate, earnings for corporations are expected to grow.

Simplified Accounting

The TCJA allows more businesses (with less than $25 million in annual sales) to use a simpler accounting technique—the cash method of accounting, where a business recognizes revenues and expenses when money changes hands, rather than when a deal is struck (the accrual method).

Pass-Through Entities

Currently, the net income of a pass-through entity (such as a partnership, S corporation, LLC, or sole proprietorship) is effectively taxed at an individual tax rate. Beginning in 2018, the TCJA tax rates for individuals are generally lowered over seven brackets—featuring a top tax rate of 37 percent. To offset the possibility that a small business owner might now end up paying higher-than-corporate-rate taxes (21 percent), the TCJA allows for a 20 percent deduction on income for pass-through entities—subject to certain limitations. The TCJA does include a rule to ensure small business owners don't "game" the system. Two main hurdles for claiming the full 20 percent deduction, "Specified Service Businesses" and "Wage and Capital Limit," must be met or the deduction may be reduced—or even eliminated.

Taxpayers who have income below the lower income threshold ($157,500 for individuals and $315,000 for married taxpayers filing jointly) have no worries at all. They are entitled to the full deduction. However, individuals in certain service professions that are traditionally high-paid positions (for example, physicians or attorneys) may not qualify for any deduction.

Inflation

Income levels will rise each year with inflation, but they will rise more slowly than in the past. The TCJA will use the Chained Consumer Price Index (C-CPI)—a slower measure of inflation than the Consumer Price Index (CPI)—to adjust income thresholds, deduction amounts, and credit values. This will be done to prevent "bracket creep," when people are pushed into higher income tax brackets (or have reduced value from credits or deductions) due to inflation, instead of any increase in real income.

Standard Deduction and Personal Exemption

The standard deduction has almost doubled, which will prompt fewer people to itemize taxes. For single filers, the standard deduction has increased from $6,350 to $12,000. For married couples filing jointly, the standard deduction has increased from $12,700 to $24,000. The personal exemption for 2018 is eliminated.

Alternative Minimum Tax

The alternative minimum tax, or AMT, was implemented to ensure that high-income earners paid their fair share of taxes, regardless of how many deductions they could claim. Essentially, higher-income households need to calculate their taxes twice—once under the standard tax system and once under the AMT—and pay whichever is higher.

Under the TCJA, fewer people will have to deal with the AMT. The exemption has been raised to $70,300 for singles and $109,400 for married couples. The exemptions phase out at $500,000 for singles and $1 million for joint. The exemption will revert to pre-TCJA levels in 2026, if Congress allows them to lapse.

Section 179

The Section 179 deduction that allows small businesses an immediate break on purchases of equipment doubles to $1 million. The phase-out threshold increases to $2.5 million. Use caution, though. The maximum allowance is still limited to the amount of income from business activity. And note also, these amounts will be indexed for inflation after 2018.

In recent years, the percentage for first-year "bonus depreciation" deductions fluctuated, complicating tax planning. The TCJA hikes the bonus depreciation deduction from 50 percent to 100 percent through 2022, and then gradually phases out the deduction over the next five years—unless another Congress revives it. The deduction has also been expanded to include used property. To qualify, the equipment must have been purchased after September 27, 2017, and before January 1, 2023.

Mileage

For business use of a car, the Internal Revenue Service has set the standard mileage rate at 54.5 cents per mile—up one cent from 2017. The mileage rate is one of two methods for accounting the business use of a vehicle. The second method is the deduction of actual expenses, where an owner must calculate the percentage of miles the car is driven for business and apply that percentage to vehicle expenses (such as fuel, maintenance, repairs, insurance, depreciation, and lease payments).

Health Care

Most company health-care plans are set for 2018, but there will be some changes when choosing policies that begin later this year or in 2019. Business owners who want to sign up for group insurance through the government's Small Business Health Options Program (SHOP) must do so through a health insurance agent or broker—or directly through an insurance company—and will no longer be able to sign up through the government website, Healthcare.gov. However, the site can still be visited to get information. The TCJA also ends the requirement that individuals buy health insurance beginning in 2019.

Medical Expenses

The medical expense deduction has been expanded for two years. In that time, filers can deduct medical expenses adding up to more than 7.5 percent of adjusted gross income, which is down from 10 percent in past years.

iStock.

Phased-Out Deductions

Entertainment expenses

Transportation fringe benefits—including mass transit passes, commuter vehicles, and parking privileges (If employers provide these benefits, however, they remain tax free to employees.)

Employer-paid wages paid for family or medical leave after 2019

Personal exemptions

Tax preparation deduction

Losses sustained due to a fire, storm, shipwreck, or theft not covered by insurance (Now through 2025, losses can be claimed if they result from an official national disaster.)

Moving expenses, except for members of the military

Interest on home equity lines of credit (Current mortgage holders are not affected.)

Alimony payments (This change begins in 2019 for divorces signed in 2018.)

Other Changes

State and local tax deduction (SALT) remains in place for those who itemize their taxes, but now there is a $10,000 cap. Taxpayers must choose between property taxes and income or sales taxes.

Child tax credit has doubled to $2,000 for children under 17. It is also available, in full, to more people. The entire credit can be claimed by single parents who make up to $200,000 and married couples who make up to $400,000. Parents who don't earn enough to pay taxes can claim the credit up to $1,400.

Taxpayers can claim a $500 temporary credit for non-child dependents, like elderly parents, children over age 17, or adult children with a disability. The TCJA allows a $500 credit for each non-child dependent. The credit helps families caring for elderly parents.

Student loan interest, which is up to $2,500 per year, is safe.

Parents can use 529 savings plans for tuition at private and religious K-12 schools, as well as college tuition. The funds can also be used for expenses for home-schooled students.

Small Business Health Options Program (SHOP)

What's changing with SHOP in 2018?1

Instead of using healthcare.gov to choose a plan and enroll, you will work with an insurance company or a SHOP-registered agent or broker. You will also pay your premiums through your agent, broker, or insurance company. You will not make payments through the website.

If you are enrolling for the first time (or you've experienced a gap in coverage), visit healthcare.gov to verify your eligibility.

Offering SHOP coverage is generally the only way for small businesses to save with the Small Business Health Care Tax Credit. For more information, visit www.healthcare.gov.

You can still use HealthCare.gov to confirm that your business is eligible for SHOP, browse plans and prices (www.healthcare.gov/see-plans/#/small-business), and find useful resources for enrolling in coverage.

You can use your current SHOP-registered agent or broker or find a new one in your area through the Find Local Help tool.

Questions? Contact the SHOP Call Center at 800-706-7893 weekdays from 9:00 a.m.-7:00 p.m. Eastern time.